Opening a medical or dental practice represents one of the most rewarding milestones in a healthcare professional’s career. It is also one of the most significant financial commitments many physicians and dentists will ever undertake. Whether you are launching your first practice, acquiring an established office, adding another provider, expanding into a larger facility, purchasing advanced technology, or opening a second location, every major growth decision requires more than clinical expertise—it requires sound business strategy, careful financial planning, and access to the right financing.

For many healthcare professionals, financing comes through a loan guaranteed by the U.S. Small Business Administration (SBA). SBA loans have helped thousands of physicians and dentists transform entrepreneurial ambitions into thriving healthcare practices by providing flexible financing for startups, acquisitions, real estate, equipment purchases, leasehold improvements, working capital, and business expansion.

Yet many applicants approach the financing process with a common misconception: that loan approval depends primarily on credit scores, collateral, production history, or years of clinical experience.

Those factors certainly matter. However, lenders are evaluating something much broader.

They want confidence that the practice will become a financially sustainable business capable of generating sufficient cash flow to cover its operating expenses and repay the loan over many years. They want to understand not only who the borrower is, but also how the business will compete, grow, manage risk, and adapt to changing market conditions.

Long before a lender reviews tax returns, financial statements, or collateral documentation, one document often shapes that first impression more than any other:

A professionally developed business plan.

Your Business Plan Is Often Your First Interview With the Bank

Many physicians and dentists believe the first meeting with a lender begins when they walk into a bank or schedule a virtual appointment with a loan officer. In reality, that conversation often begins long before the first handshake.

Your business plan introduces your practice to the lender before you have the opportunity to explain your vision in person. It demonstrates your preparation, professionalism, strategic thinking, and understanding of the business you intend to build.

A lender reviewing a financing package is asking questions such as:

-

- Does this applicant understand the healthcare marketplace?

-

- Are the financial projections realistic and supported by data?

-

- Has local competition been carefully evaluated?

-

- Will projected patient volume generate adequate cash flow?

-

- Is there sufficient working capital to navigate the early stages of growth?

-

- Does management have a realistic operational strategy?

The business plan should answer these questions with confidence and credibility. A well-prepared plan does more than satisfy a lending requirement—it helps establish trust between the borrower and the financial institution.

Unfortunately, many loan applicants underestimate its importance. Generic templates, internet-generated business plans, or documents prepared without thoughtful financial analysis often fail to communicate the depth of planning lenders expect when evaluating six- or seven-figure financing requests.

Clinical Expertise and Business Success Are Different Disciplines

Physicians and dentists dedicate years to developing exceptional clinical skills. Their education emphasizes patient care, diagnosis, treatment planning, and evidence-based medicine. Very little of that training focuses on evaluating market opportunities, preparing financial forecasts, managing operational performance, or building a long-term business strategy.

Owning a successful healthcare practice requires balancing two very different responsibilities. On one side is the delivery of outstanding patient care. On the other hand, operating a financially healthy business that supports employees, invests in technology, adapts to regulatory changes, and generates consistent profitability.

That balance becomes especially important when seeking financing.

Lenders recognize that outstanding clinicians do not automatically possess extensive experience in business planning or financial modeling. Rather than expecting healthcare providers to become experts in every aspect of business management, they look for evidence that the practice has been thoughtfully planned and supported by professional analysis.

A comprehensive business plan bridges that gap by translating clinical vision into a credible business strategy supported by measurable financial assumptions.

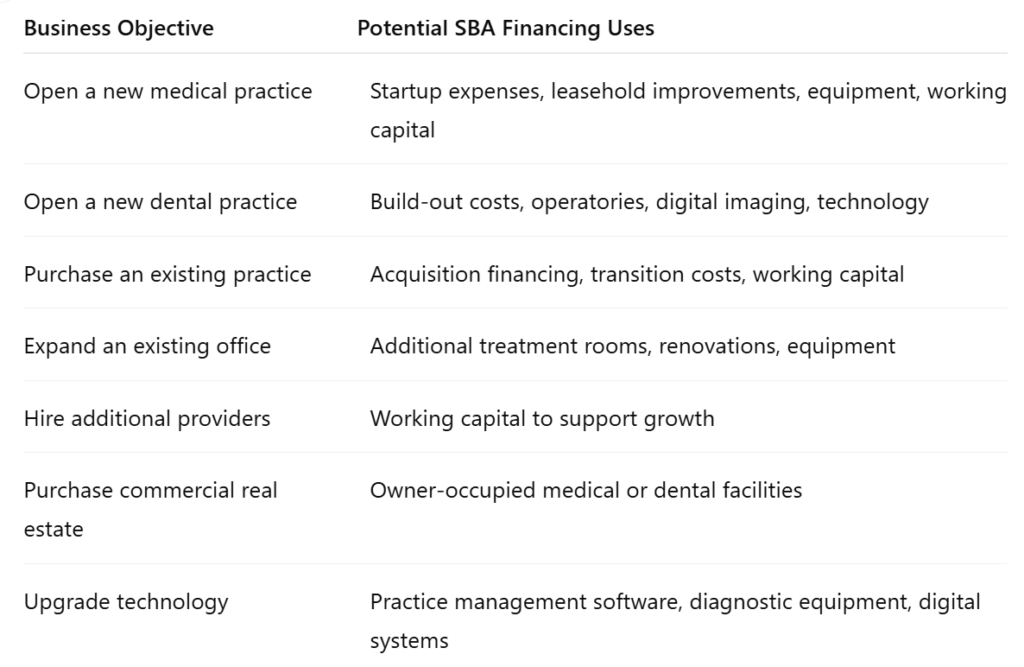

SBA Financing Supports More Than New Practice Startups

One of the greatest advantages of SBA financing is its versatility. While many people associate SBA loans with startup businesses, healthcare professionals use SBA financing throughout the entire lifecycle of their practices.

A well-structured SBA loan may help finance:

Regardless of the purpose, lenders evaluate every request from the same perspective: Does this investment make sound business sense?

That question cannot be answered solely through historical tax returns or credit reports. It requires a thoughtful analysis of market conditions, operational planning, financial performance, and long-term strategy—precisely the role of a comprehensive business plan.

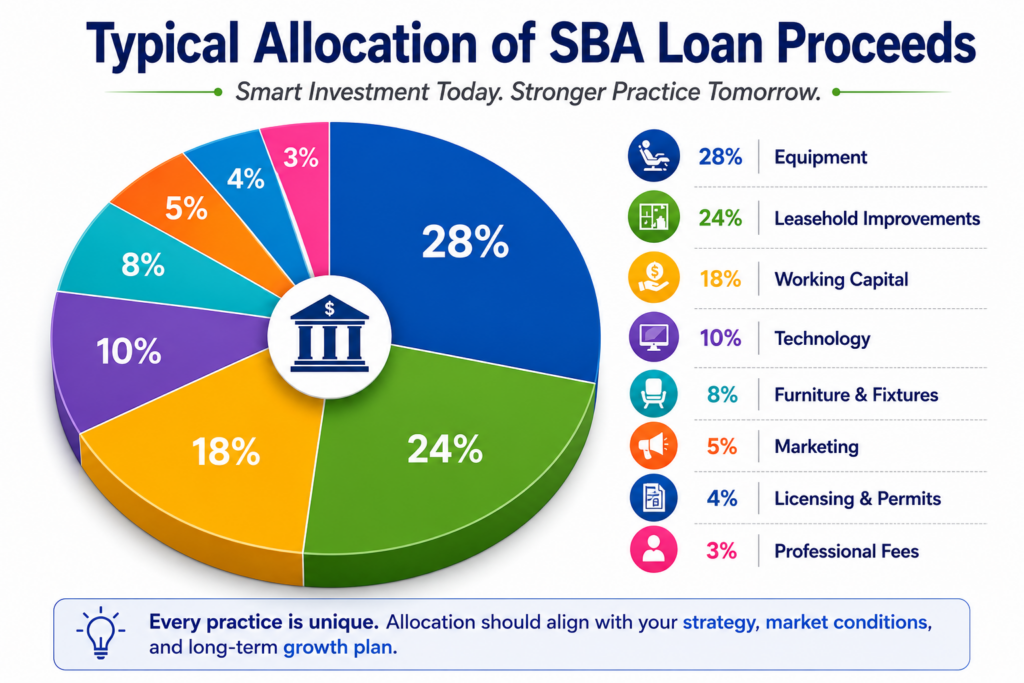

How Are SBA Loan Proceeds Typically Used?

Although every medical and dental practice has unique financing needs, lenders expect borrowers to have a clear understanding of how loan proceeds will be invested. A thoughtful allocation of capital helps ensure that sufficient funds are available not only to open the practice but also to operate successfully during the critical early months. The following chart illustrates a typical allocation of SBA loan proceeds for a startup or practice acquisition.

The percentages shown above represent a typical financing structure and should not be viewed as a one-size-fits-all solution. Every practice has different equipment requirements, build-out costs, staffing needs, and working capital demands. Developing the appropriate financing strategy requires careful planning, realistic financial analysis, and a comprehensive business plan that aligns loan proceeds with the practice’s long-term objectives.

Banks Do Not Finance Ideas—They Finance Well-Planned Businesses

Every SBA lender understands that healthcare is one of the most stable industries in the United States. People will always need physicians, dentists, specialists, and other healthcare providers. However, lenders also recognize that not every healthcare practice becomes financially successful. Excellent clinicians sometimes struggle because they underestimate the business challenges associated with ownership.

From the lender’s perspective, every loan represents an investment in the practice’s future performance. While the SBA may guarantee a portion of the loan, the lending institution remains responsible for making prudent credit decisions. Consequently, loan officers and underwriters carefully evaluate whether the proposed practice has a realistic opportunity to generate sufficient revenue, maintain healthy cash flow, and meet its financial obligations.

A lender is not simply asking whether the applicant deserves financing. Instead, the lender is evaluating whether the proposed business has been thoughtfully planned and whether the financial assumptions are supported by credible analysis.

Some of the questions lenders commonly consider include:

-

- Is there sufficient patient demand within the proposed service area?

-

- Does the location provide access to the target patient population?

-

- How competitive is the local healthcare market?

-

- Are projected collections supported by realistic production assumptions?

-

- Can projected cash flow comfortably support payroll, overhead, operating expenses, and loan payments?

-

- Has the owner planned for slower-than-expected patient growth?

-

- Is adequate working capital available during the startup or transition period?

-

- Does management have a practical operational strategy to support long-term growth?

Each of these questions should be addressed in a comprehensive business plan. When those answers are supported by reliable financial analysis and realistic assumptions, the lender gains confidence that the practice has been planned rather than imagined.

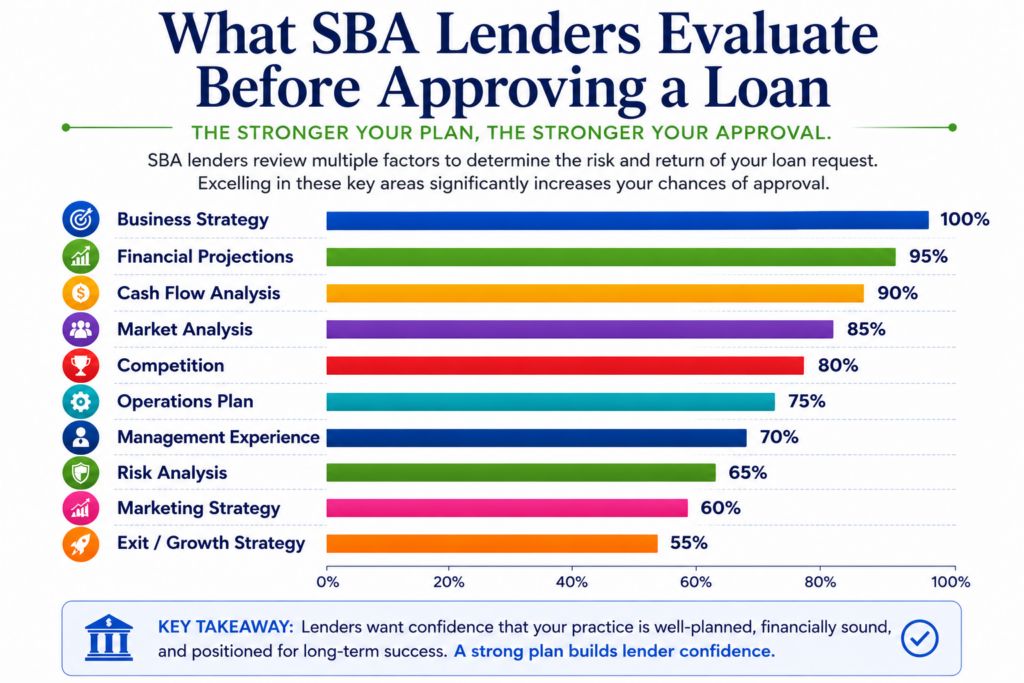

What Do SBA Lenders Really Evaluate?

While every lender has its own underwriting guidelines, most SBA lenders evaluate many of the same core business fundamentals. They are looking beyond credit scores and collateral to assess whether the proposed practice has been strategically planned, is financially viable, and is positioned for long-term success. The following chart summarizes the key factors that influence lenders’ confidence during the underwriting process.

The categories shown above should not be viewed as independent requirements. They work together to tell the overall story of your practice. A sound business strategy, realistic market analysis, thoughtful operational planning, and effective risk management support strong financial projections. A comprehensive business plan integrates these elements into a single document that demonstrates preparation, professionalism, and long-term vision—qualities every lender values.

The Business Plan Is More Than a Lending Requirement

Many applicants view the business plan as just another item on the lender’s checklist—a document they complete simply because the bank requests it. That perspective significantly undervalues one of the most important planning tools a business owner will ever develop.

A professionally prepared business plan serves several purposes simultaneously.

First, it provides lenders with a clear understanding of the business opportunity and demonstrates that the applicant has carefully evaluated the investment’s risks.

Second, it helps owners organize their own thinking. Many business concepts appear financially attractive until they are subjected to detailed financial modeling and operational analysis. A business plan forces important questions to be answered before substantial financial commitments are made.

Third, it serves as a roadmap for managing the practice once financing has been approved. Rather than sitting in a file cabinet after the loan closes, a well-developed business plan becomes a valuable management resource that guides future decision-making.

An effective business plan for a medical or dental practice typically addresses:

-

- Executive summary

-

- Practice overview

-

- Ownership and management structure

-

- Market and demographic analysis

-

- Competitive evaluation

-

- Services offered

-

- Marketing and patient acquisition strategy

-

- Operational plan

-

- Staffing strategy

-

- Technology requirements

-

- Revenue projections

-

- Expense forecasts

-

- Cash flow projections

-

- Break-even analysis

-

- Funding requirements

-

- Sources and uses of loan proceeds

-

- Risk assessment

-

- Long-term growth strategy

Each section contributes to the lender’s overall understanding of the business. Together, they create a comprehensive picture of how the practice intends to operate, compete, and achieve financial success.

Why Financial Projections Matter More Than Many Applicants Realize

Among all sections of a business plan, financial projections often receive the greatest scrutiny from lenders. This is understandable because future cash flow ultimately determines whether a loan can be repaid.

Unfortunately, many applicants rely on overly optimistic assumptions when preparing their financial forecasts. They estimate patient growth without supporting data, underestimate operating expenses, overlook seasonal fluctuations, or fail to include adequate working capital during the startup period.

Experienced lenders recognize these weaknesses almost immediately.

Strong financial projections are not designed to impress lenders with unrealistic growth. Instead, they demonstrate thoughtful planning, conservative assumptions, and a clear understanding of how the practice is expected to perform under different operating conditions.

A comprehensive financial model should consider factors such as anticipated patient volume, reimbursement patterns, production capacity, staffing costs, occupancy expenses, equipment financing, technology investments, insurance costs, marketing expenses, and ongoing operating overhead.

More importantly, the financial projections should align with the operational strategy described throughout the remainder of the business plan. If projected revenue assumes rapid patient growth, the marketing strategy and staffing plan should demonstrate how that growth will realistically occur.

Consistency throughout the business plan strengthens credibility and reinforces confidence in the proposed financing request.

Purchasing an Existing Practice Requires More Than Reviewing Revenue

Acquiring an established medical or dental practice is often perceived as less risky than starting a practice from the ground up. Existing patients, established referral relationships, experienced staff, and historical financial records can certainly reduce some uncertainties associated with a startup.

However, acquisitions introduce an entirely different set of financial and operational considerations.

Historical revenue alone does not determine whether a practice represents a sound investment. Buyers must evaluate profitability, overhead expenses, lease obligations, equipment replacement needs, employee retention, patient demographics, referral sources, technology infrastructure, reimbursement trends, and transition planning.

For example, two dental practices with identical annual collections may achieve dramatically different profitability levels depending on staffing efficiency, facility costs, payer mix, and operating expenses.

Similarly, a medical practice may appear financially healthy until future equipment replacement costs, deferred maintenance, or declining reimbursement rates are incorporated into the financial analysis.

A comprehensive business plan evaluates these variables before financing decisions are made, allowing both the buyer and the lender to understand the acquisition’s long-term financial outlook better.

The objective is not simply to purchase an existing practice—it is to purchase one capable of producing sustainable, long-term value.

A Strong Business Plan Can Save Thousands of Dollars

Many practice owners focus exclusively on whether a business plan will improve the likelihood of loan approval. While that is certainly an important objective, the greatest financial value often comes from the planning process itself.

A carefully developed business plan can identify financial risks before they become expensive mistakes.

It may reveal that the requested loan amount should be adjusted to improve cash flow. It may identify underestimated startup costs that could otherwise create immediate financial pressure. It may demonstrate that additional working capital is necessary during the early months of operation. It may even uncover operational inefficiencies that can be corrected before the practice opens its doors.

In many cases, these insights save practice owners far more money than the cost of preparing the business plan itself.

Business planning should therefore be viewed as an investment in better decision-making rather than simply an administrative requirement imposed by a lender.

The strongest healthcare businesses are rarely built through guesswork. They are built through careful analysis, informed decision-making, and strategic planning long before the first patient is scheduled.

How California Business Consulting Can Help

California Business Consulting helps medical and dental practices strengthen business performance through strategic planning, operational improvement, financial analysis, workflow optimization, KPI reporting, practice startups, acquisitions, expansions, SBA and commercial loan business plans, financial forecasting, organizational efficiency, and long-term growth strategies. Whether you are opening a new practice, purchasing an existing office, expanding your operations, or improving profitability, we provide practical, data-driven solutions that help you make informed decisions and build sustainable success. To learn more or schedule a confidential consultation, contact Dr. Michael Kamali, DBA, MBA, ChFC, at (310) 541-1000 or visit https://calbizconsulting.com.