Opening a medical or dental practice in California can be one of the most important professional and financial decisions of a physician’s or dentist’s career. It is more than renting office space, buying equipment, hiring staff, and opening the doors. A successful practice requires a clear business strategy, realistic financial projections, strong operational planning, and a lender-ready business plan that explains how the practice will generate revenue, control expenses, manage cash flow, and repay financing.

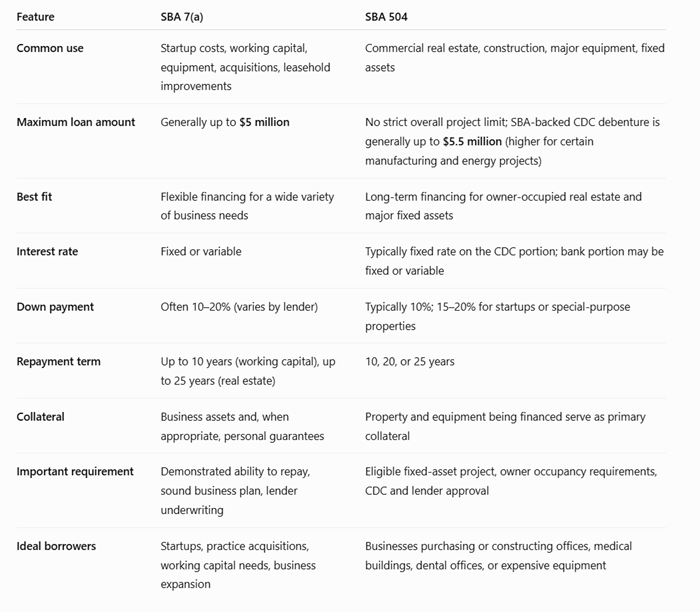

For many healthcare professionals, SBA 7(a) and SBA 504 loans can be valuable financing tools. The SBA 7(a) loan program is the SBA’s primary business loan program. It can be used for many business purposes, including working capital, equipment, leasehold improvements, business acquisition, and startup costs. The SBA states that the maximum 7(a) loan amount is generally $5 million. The SBA 504 program is designed for major fixed assets such as real estate, construction, and large equipment, with a maximum SBA loan amount generally up to $5.5 million. Loan approval, terms, eligibility, and underwriting are determined by participating lenders and SBA requirements, so a strong plan matters.

At California Business Consulting, we help physicians, dentists, and healthcare entrepreneurs prepare comprehensive SBA business plans, detailed financial projections, startup budgets, cash flow forecasts, market analysis, and strategic planning documents that support more informed financing discussions. We do not make loans or guarantee approval. Our role is to help practice owners present a stronger, more organized, and more financially credible business case to lenders.

🏥 The Real Question Is Not Only “Can I Get a Loan?”

Many doctors and dentists begin the process by asking, “How much can I borrow?” That is a reasonable question, but it is not the first question a lender will ask.

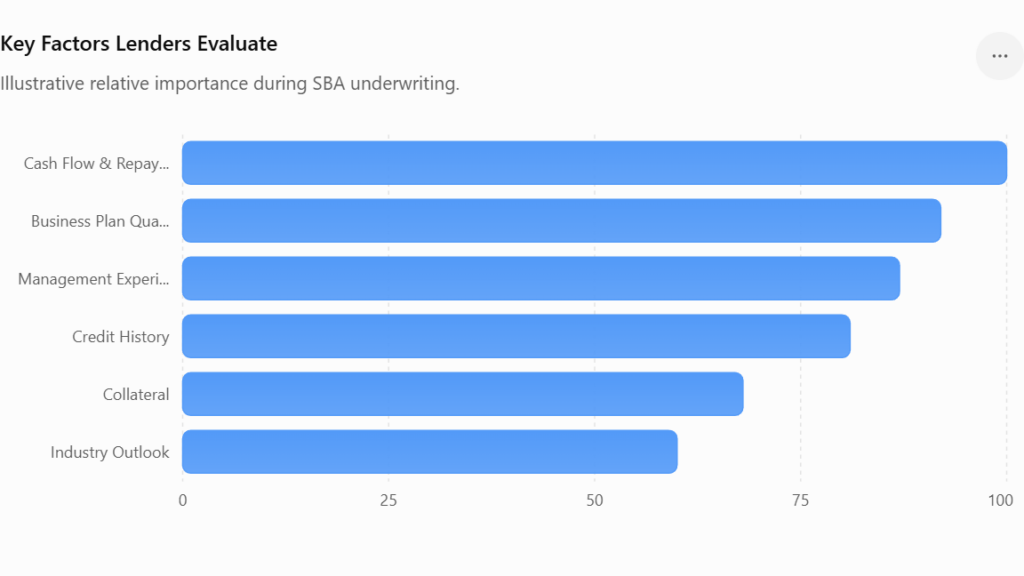

A lender usually wants to understand whether the proposed practice can become a financially viable business. That means reviewing the borrower’s experience, location, startup budget, projected patient volume, insurance mix, staffing plan, operating expenses, working capital needs, and the practice’s ability to repay debt with future cash flow.

A beautiful office does not guarantee a successful practice. Expensive equipment does not guarantee profitability. A strong clinical background does not automatically create a sound business model. The practice must be planned as a business from the beginning.

That is why the business plan becomes so important. A lender-ready business plan explains the practice concept, the market opportunity, the services offered, the competitive landscape, the startup budget, the marketing strategy, the staffing model, and the financial projections. It helps translate a clinical vision into a business case.

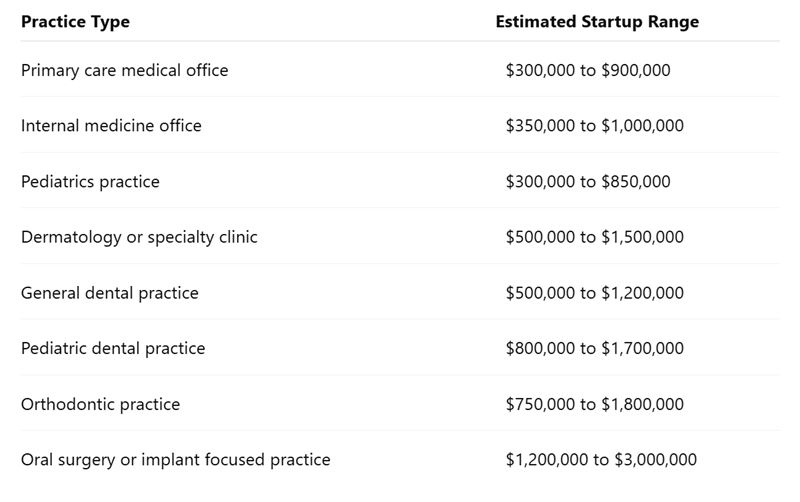

💰 Estimated Cost of Opening a Medical or Dental Practice in California

Startup costs vary widely depending on location, specialty, size, equipment, tenant improvements, technology, staffing, and whether the owner is starting from scratch or acquiring an existing practice. Southern California markets such as Beverly Hills, Irvine, Newport Beach, Pasadena, Glendale, Long Beach, San Diego, Riverside, and Santa Clarita can differ significantly in rent, build-out costs, competition, and patient demographics.

These are planning ranges, not guarantees. A small medical office in Riverside may require a very different investment than a specialty dental practice in Beverly Hills or Newport Beach. The purpose of the startup budget is to identify the real funding requirement before the owner signs a lease, orders equipment, or approaches a lender.

Typical startup costs may include leasehold improvements, equipment, furniture, computers, software, imaging systems, supplies, licensing, insurance, marketing, legal fees, accounting, website development, payroll reserves, and working capital. For dental practices, operatories, compressors, sterilization equipment, X-ray systems, chairs, cabinetry, and digital technology can materially increase the startup budget. Medical offices, examination rooms, diagnostic equipment, electronic health record systems, medical supplies, compliance needs, and specialty equipment can substantially affect financing requirements.

💡 Consultant’s Perspective

Many practice owners underestimate working capital. They budget for construction and equipment but forget that the practice may need several months to build patient volume, submit claims, receive reimbursement, train staff, and stabilize operations. A thoughtful financial plan should include enough working capital to support the practice during the early months when cash flow is still developing.

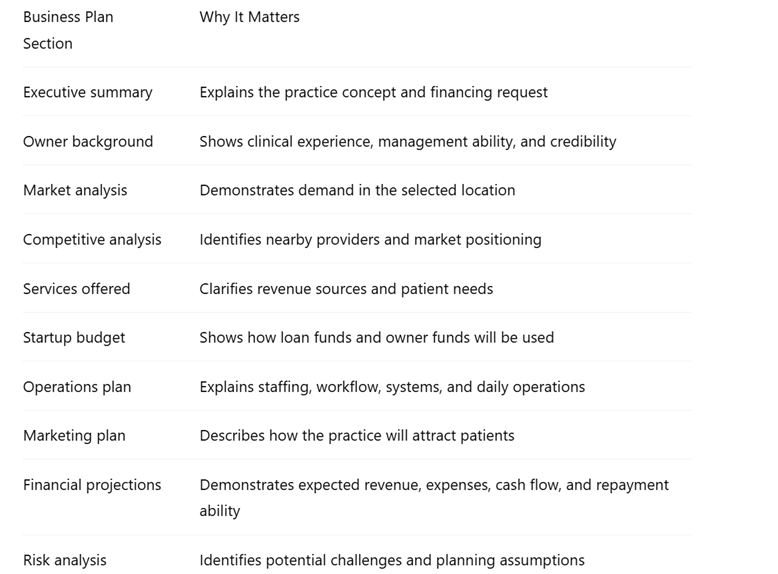

📋 Why Lenders Often Require a Business Plan

A business plan is not just a formality. It is one of the main tools lenders use to evaluate whether the practice has a realistic path to success. Banks and SBA participating lenders want to know how the owner plans to use the funds, how revenue will be generated, how expenses will be controlled, and how repayment will occur.

A strong SBA business plan for a medical or dental practice should typically include:

For physicians and dentists, the business plan must be practical and financially grounded. Please avoid making it sound like a generic template. It should reflect the realities of healthcare practice operations, payer mix, patient acquisition, staffing, lease obligations, equipment investment, and cash flow timing.

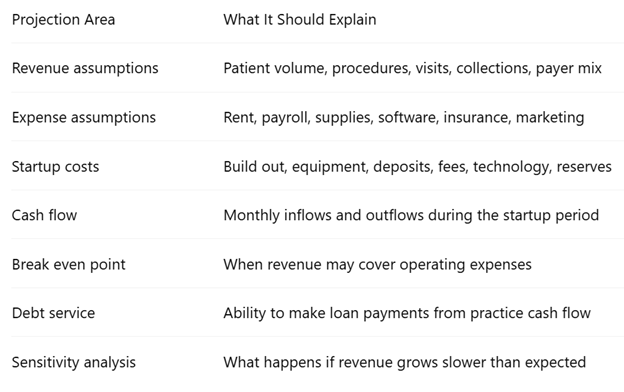

📊 Financial Projections Are Often the Heart of the SBA Package

For many lenders, the financial projections are among the most important parts of the package. The projections help lenders evaluate whether the practice can cover operating expenses and debt service while maintaining sufficient cash flow to operate.

A complete projection package may include projected income statements, cash flow statements, balance sheets, startup cost schedules, working capital assumptions, break-even analysis, debt service analysis, and sensitivity analysis.

Financial projections should be realistic, not overly optimistic. A lender may become concerned if the projections assume immediate profitability, very high patient volume, unusually low payroll, or insufficient marketing. Strong projections show the logic behind the numbers. They help explain how the practice will move from startup to stable operations.

Caption:

Figure 1. SBA 7(a) loans provide flexible financing for multiple business needs, making them especially suitable for new and expanding medical and dental practices.

💡 Consultant’s Perspective

The most persuasive projections are not the most aggressive projections. They are the projections that make sense. Lenders want to see assumptions that are reasonable, well-documented, and aligned with the actual business model. A conservative and well-supported financial forecast can be more credible than an inflated projection that appears designed solely to secure approval.

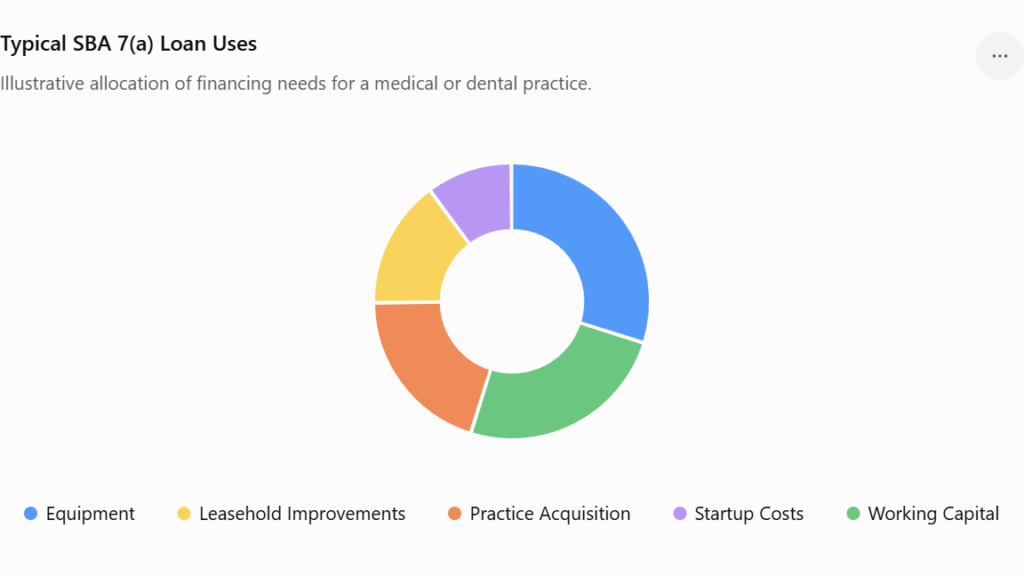

🏦 How SBA 7(a) Loans Can Help Medical and Dental Startups

Medical and dental practices often use SBA 7(a) loans because they can support a broad range of business needs. For a startup practice, a 7(a) loan may help finance leasehold improvements, equipment, furniture, working capital, software, inventory, professional fees, and other eligible startup costs. It may also be used for practice acquisitions, depending on the lender and transaction structure.

Figure 2. Cash flow and repayment capacity generally carry greater weight than collateral alone during SBA loan underwriting.

For example, a dentist opening a new practice in Irvine may need funding for tenant improvements, dental chairs, digital imaging, sterilization systems, software, supplies, marketing, and payroll reserves. A physician opening an internal medicine office in Pasadena may need funds for examination rooms, electronic health records, diagnostic equipment, staffing, insurance, marketing, and working capital. In both cases, the lender will want to understand the business plan, the startup budget, and the repayment strategy.

SBA 7(a) financing can be useful because it may offer longer repayment terms than some conventional business loans, depending on the use of funds and lender structure. However, it is still a loan that must be repaid, and the lender will underwrite the borrower, the business concept, collateral, credit, cash flow, and other risk factors.

🏢 How SBA 504 Loans Can Help Practice Owners Buy Real Estate or Major Equipment

SBA 504 financing is generally designed for major fixed assets that support business growth, such as owner-occupied commercial real estate, construction, and large equipment. For a healthcare professional who wants to purchase a medical office building, dental office condo, or property for long-term practice use, an SBA 504 loan may be worth exploring.

A dermatologist in Beverly Hills may consider SBA 504 financing to purchase a medical office property. A dental group in Newport Beach may use 504 financing to acquire and improve a building for a multi-operatory practice. A specialty clinic in San Diego may evaluate SBA 504 financing to support expansion at a larger facility.

The 504 structure is different from a typical 7(a) loan because it involves a participating lender and a Certified Development Company. It can be attractive for real estate and fixed-asset projects, but it requires careful planning, documentation, and an eligibility review.

📍 Southern California Practice Startup Scenarios

A family physician in Irvine may need $650,000 to open a modern primary care office with four examination rooms, electronic health records, furniture, staff training, website development, and working capital. A lender would likely want to see how patient volume will grow, how reimbursement will be collected, and when the practice is expected to reach break-even.

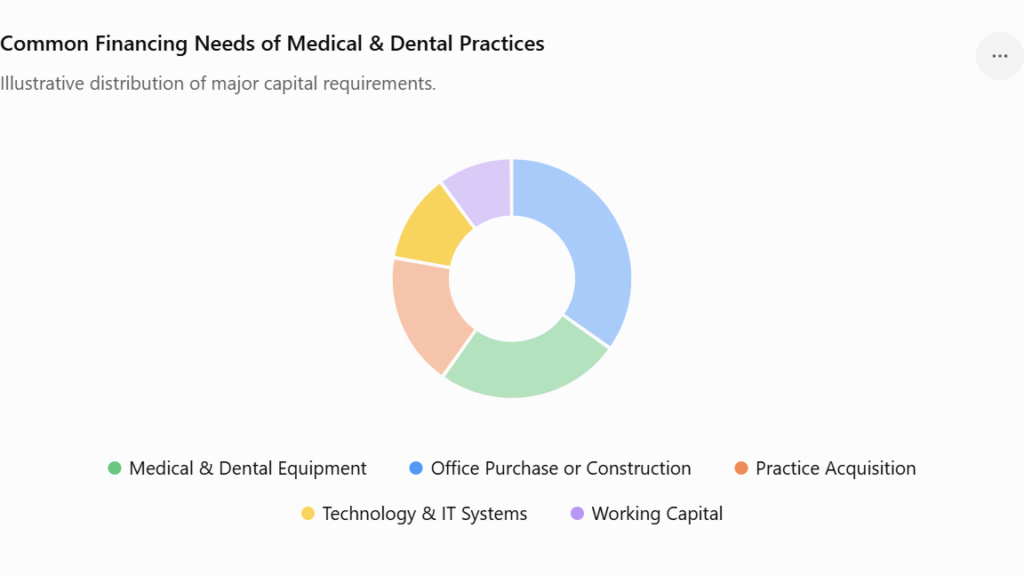

Figure 3. Illustrative distribution of common financing needs for medical and dental practices. Actual financing requirements vary depending on practice size, specialty, growth stage, and business objectives.

A dentist in Pasadena may need $900,000 to build a general dental practice with four operatories, digital X-rays, sterilization equipment, practice management software, tenant improvements, and marketing. The business plan should explain local competition, patient demographics, service mix, expected collections, and staffing requirements.

A pediatric dentist in Long Beach may require $1.3 million because pediatric dental offices often require specialized equipment, child-friendly design, additional staff training, and a larger marketing effort. In this case, the lender may focus heavily on startup budget discipline and the owner’s ability to build referral relationships.

A dermatologist in Beverly Hills may need financing for a specialty practice with higher equipment costs, premium lease rates, and a more competitive market. The financial projections should show how service pricing, patient demand, staffing, and fixed costs support the proposed financing structure.

A dental specialist in San Diego may evaluate whether to lease space with a lower initial investment or purchase a property using SBA 504 financing. The decision affects monthly obligations, long-term equity, cash reserves, and the overall risk profile of the practice.

These scenarios show why there is no single financing answer for every healthcare startup. The right structure depends on the practice type, location, owner resources, growth strategy, and lender requirements.

⚠️ Common Mistakes That Delay SBA Financing

Many medical and dental practice financing applications are delayed due to an incomplete business case. The lender may like the borrower and still need more information before moving forward.

Caption:

Figure 3. Healthcare practices often require financing for real estate, equipment, acquisitions, technology investments, and operating capital.

Common mistakes include unrealistic revenue projections, incomplete startup budgets, weak market analysis, underestimating working capital needs, unclear use of loan proceeds, limited explanation of the owner’s experience, missing documents, vague marketing plans, and financial projections that do not align with the business plan.

Another common mistake is approaching lenders before the financing package is ready. A physician or dentist may have a strong concept but still struggle to answer basic lender questions about patient volume, break-even timing, payroll, insurance reimbursement, lease obligations, and cash flow. This can create delays, confusion, and unnecessary frustration.

A lender-ready business plan does not guarantee approval, but it can make the conversation more organized and professional. It helps the lender understand the practice and helps the owner clarify the financial realities before making major commitments.

✅ How California Business Consulting Helps

California Business Consulting works with physicians, dentists, healthcare professionals, and small business owners who need strategic business planning, SBA business plans, financial projections, startup budgets, cash flow analysis, and operational planning.

For medical and dental practice startups, we can help develop the planning documents that lenders commonly expect to review, including a comprehensive business plan, three- to five-year financial projections, use of funds schedule, startup budget, market overview, competitive analysis, staffing assumptions, revenue model, operating expense assumptions, and financial narrative.

Our work is designed to help clients think clearly, plan realistically, and communicate their business case more effectively. The goal is not simply to prepare documents. The goal is to help the practice owner understand the financial and operational foundation of the proposed business before making one of the largest investments of their professional career.

❓ Frequently Asked Questions

Do SBA lenders require a business plan for medical or dental practice financing?

Many lenders request a business plan, especially for startups, acquisitions, and large financing requests. A business plan helps explain the practice concept, startup budget, market opportunity, financial projections, and repayment strategy.

Can SBA 7(a) loans be used for dental or medical practice startups?

SBA 7(a) loans may be used for many business purposes, including eligible startup costs, equipment, leasehold improvements, working capital, and acquisitions. Final eligibility and approval depend on the lender’s underwriting and SBA requirements.

Is SBA 504 better than SBA 7(a)?

Neither program is automatically better. SBA 7(a) is often more flexible for startup costs and working capital, while SBA 504 is generally more focused on real estate, construction, and major fixed assets. The right choice depends on the project.

How much does it cost to open a dental practice in California?

A general dental practice may require approximately $500,000 to $1.2 million, while specialty or pediatric dental practices can require more. Location, office size, equipment, and build-out needs can significantly affect the total cost.

How much does it cost to open a medical practice in California?

A small medical office may require approximately $300,000 to $900,000, while specialty clinics can exceed $1 million depending on equipment, leasehold improvements, staffing, and working capital.

Does California Business Consulting provide loans?

No. California Business Consulting is not a lender and does not guarantee approval for financing. We help clients prepare business plans, financial projections, startup budgets, and strategic planning documents that support financing discussions with lenders.

📞 Ready to Plan Your Medical or Dental Practice Startup?

Opening a medical or dental practice in California requires more than enthusiasm and clinical experience. It requires disciplined planning, realistic financial projections, a clear understanding of startup costs, and a professional business plan that helps lenders evaluate the opportunity.

If you are planning to open, acquire, or expand a medical or dental practice, California Business Consulting can help you prepare a lender-ready business plan, SBA financial projections, startup budget, and strategic planning package to support informed decision-making and stronger conversations with lenders.

Contact California Business Consulting to discuss your medical or dental practice startup planning needs.

https://calbizconsulting.com

Website: CalBizConsulting.com

About the Author

Dr. Michael Kamali, DBA, MBA, ChFC, is the founder of California Business Consulting. He helps physicians, dentists, healthcare organizations, and growing businesses develop strategic business plans, SBA business plans, financial projections, operational improvement strategies, and long-term growth plans. His background combines business strategy, financial analysis, banking, lending, consulting, and executive decision support to help clients evaluate business opportunities with greater clarity and discipline.

Related Consulting Services

- Business Planning Services

https://calbizconsulting.com/services/business-planning-services/ - SBA Business Plans

https://calbizconsulting.com/services/sba-business-plans/ - Business Strategy Consulting

https://calbizconsulting.com/services/business-strategy-consulting/ - Financial Analysis & Decision Support

https://calbizconsulting.com/services/financial-analysis-decision-support/ - Healthcare Consulting

https://calbizconsulting.com/services/healthcare-consulting/ - Dental Practice Consulting

https://calbizconsulting.com/services/dental-practice-consulting/ - Operations Consulting

https://calbizconsulting.com/services/operations-consulting/ - Process Improvement & Organizational Efficiency

https://calbizconsulting.com/services/process-improvement-organizational-efficiency/

Related Industries

- Dental Practices

https://calbizconsulting.com/industries/dental-practices/ - Medical Offices

https://calbizconsulting.com/industries/medical-offices/ - Healthcare Organizations

https://calbizconsulting.com/industries/healthcare-organizations/ - Professional Service Firms

https://calbizconsulting.com/industries/professional-service-firms/ - Emerging & Growth Companies

https://calbizconsulting.com/industries/emerging-growth-companies/